An auditor can view themselves as many different personas, but up until recently ‘audit data analyst’ was not one of those personas. The truth is, I’ve always thought that this was a bit of an unfair position for auditors.

For as long as I have been involved in the accounting and finance industries, auditors have been drawing conclusions about large populations of data by using random sampling or a particular strategic lens. What has always impressed me is how a seasoned partner can spot an error deep in the numbers just by looking at the primary statements.

Embracing new data analysis techniques during audits

What’s most interesting today is how professional data analytics techniques from other fields are being combined with traditional audit approaches. This has enabled new ways for auditors to interrogate, understand, and gain assurance during data journal entry analysis or general ledger analysis. This ranges from basic aggregation techniques such as calculating proof in totals and creating moderately complex data visualizations to machine learning techniques designed to spot unusual patterns.

Using AI-powered technology such as Ai Auditor, audit data analysis appears to be entering a new phase of progression. AI audit solutions leverage machine learning to analyze general ledgers and deliver automated risk scores across all transactions and financial data.

How the role of the data analyst is evolving with AI technology

Learning how to properly implement these technologies to evolve auditing processes and general ledger analysis requires consideration. However, I have seen many instances where these cutting-edge audit analysis technologies were able to flag truly interesting items such as the purchase of a Porsche for a company director. When one experiences these types of results with AI audit software, it’s easy to believe that the future is here for journal entry analysis. And, long gone is the day of manual data segmentation in Excel.

Many of these AI audit solutions work by building some expectation of normal within a specific pool of data. The many breakthroughs that are still occurring in data science and artificial intelligence will likely improve the machine’s sense of nuance. As more accurate models involve higher levels of complex analysis, we must, as an industry, weigh this fact against our need for explainable results.

This is not the end for analyzing audit data. Some auditors will always carry the persona of data analysts because they are inherently great at decoding data. However, perhaps that role is evolving alongside new AI audit technology. And perhaps, that’s a good thing.

Want to learn more about how auditors are using AI?

For most auditors, surviving another audit busy season can be a rough ride. Between the 60-80-hour workweeks and the constant pressure to meet deadlines, there’s little time to rest, gather with family or friends, or enjoy personal hobbies. The reality is that stress is at an all-time high during the audit busy season, and many auditors can reach the brink of burnout.

The COVID-19 pandemic and work-from-home mandates have made things harder for some. Auditors not only have to work extra-long days, but there are fewer chances to break away from the desk and get some much-needed downtime. As the lines between work and home become even more blurred, there’s a serious risk for increased mental health crises.

Auditors are also having to juggle the inherent challenges of remote audits. Everything from trying to figure how to securely access client information and ensuring cybersecurity best practices, to scouring financial data to detect rising cases of fraud put even more pressure on auditors.

Conducting effective remote audits begins with selecting the right audit tools. Everything must be considered, from how an audit team will communicate with clients to how files will be shared.

For instance, using a cloud-based AI auditing platform can simplify the sharing of financial data. Clients can quickly upload files into the secure AI platform, allowing the audit team to remotely access and analyze information. With AI power at hand, auditors can also run multiple algorithms across all client transactions simultaneously and cross-correlate data using dozens of testing criteria. This gives them a clearer picture of potential risks.

2 – Prioritize your personal wellbeing during audit busy season

Working from home for long periods of time can wreak havoc on anyone’s mental and physical health. Coupling this with the added stresses of the audit busy season, and auditors become highly susceptible to burnout.

Scheduling short bouts of exercise, yoga, or meditation each day can make a big difference. According to the Anxiety and Depression Association of America, even taking five minutes for light physical movement can reduce stress and stimulate anti-anxiety effects. Auditors who take time to prioritize self-care, get outside for walks, and use meditation apps will be able to better manage the stresses of the busy audit season. Plus, you may even produce better work.

3 – Ease the wake-up-and-work rush of the busy season

Before getting to the at-home workspace, auditors can plan some time for a burst of exercise and home-cooked breakfast or jump in the car to snag a latte at their favorite drive-through coffee shop. These small tasks bring some level of normalcy and variety to what can feel like endless days of remote auditing.

As well, setting firm boundaries around when a workday begins and ends will help auditors delineate work from quality time with family or simple relaxation. Working from home doesn’t have to mean that you’re “always on” or “always available.” This mindset is a one-way ticket to Burnout City.

4 – Re-evaluate auditing best practices

Auditing methodologies and best practices evolve constantly. This is especially true as new technologies become more widely accepted and used in auditing practices. To minimize stress and ensure the highest quality audits and risk assessments, auditors should always take some time to review any updates on audit methodologies and standards. This allows audit teams to better plan for audit engagements and ensures they’re using the most current information to handle their remote audits.

Working on remote audits while trying to meet looming deadlines is hard enough. But today, it’s become even more imperative for auditors to stay informed about the latest cyber risks and take action to prevent data breaches. The best way to do this is by partnering with transparent and trustworthy technology partners. Auditing firms should vet technology providers by asking about their cybersecurity policies and initiatives, their accreditations and certifications, and any accessible tools that ensure the highest level of resilience to cyber attacks.

Delivering quality work efficiently during the audit busy season

As another busy audit season approaches and remote audits become the new norm, auditors need to rethink how they’re going to manage the current and upcoming stresses and challenges. By implementing the right strategies and tools, auditors can better navigate the audit busy season without reaching a state of complete exhaustion. More than that, they can retain the highest quality of audits and assessments, without compromising data privacy and security.

Have you noticed that no one really calls it a “smartphone” anymore?

It’s just a phone.

The fact that it is “smart” is a given — it’s phone 1-0-1, it’s the least possible useable thingy (aka minimum viable product), it’s the baseline for customer experience.

No longer do phone users want to:

Type words in full in an SMS

Carry a phone AND a camera

Have to sit at a desktop to scroll social media endlessly

Read actual maps

Sit and wait for anything without being able to check emails/Twitter/Facebook/latest news/ browse internet/just generally ignore the world around them….

Harshly, there’s a reason why non-smartphones are now referred to as “dumb phones”.

If I consider it appropriate for my 9-year-old to have a phone of any sort in the near future, it will most certainly be one of these “dumb phones”. In fact, it will be so dumb that she finds it SO boring that she’ll only use it for emergencies (fancy that!) and avoid phone trouble traps of selfies, text neck, and cyberbullying.

What’s this got to do with AI audit?

“AI auditing” is the new “auditing”.

We’re incredibly privileged to have advances in AI technology that are being democratized by companies for real-world applications NOW. As such, we won’t have “AI audit” and “AI auditors” for much longer — we’ll simply have auditors doing auditing where the assumption, the MVP, and the baseline expectation is that they are powered by artificial intelligence, to all the significant benefit of their clients, the profession, and themselves personally.

Why?

AI auditors…

…are more efficient

A well-planned audit is an efficient audit. AI audit can, for example, risk-rate 100% of the transactions in the general ledger and sub-ledgers to produce an aggregated risk profile of the data that makes up the business’ financial statements, facilitating laser-like focus on the areas that matter.

…deliver better audit quality

Audit is an essential source of public confidence in financial reporting and hence trust in business and the wider economy. AI audit enhances quality by allowing auditors greater certainty to relay to clients:

That the financial statements are free from material misstatement

Details of any material deficiencies detected so that they can be addressed

Rather than using risk assessment and data analytics processes to find the needle in the haystack, AI audit sets the haystack on fire to discover more needles with a fraction of the effort.

…add more value

AI-powered analytics within the audit process allow auditors to surface insights perhaps not available to clients from their internal systems. With the capacity created from more efficient planning and execution, AI auditors can feed these valuable insights back to their clients, creating client “stickiness” through real value provision.

…can diversify into new service offerings

Fast emerging in the world of audit is the concept of the “continuous audit” or “continuous risk management” as a service. Imagine a more periodic peace-of-mind, or sense-check or proactive fraud-risk indicator for business owners, CFOs, audit committees, boards, and CEOs alike. Brilliant in theory but generally difficult to deliver to market commercially without some very controlled and prescriptive process or automation. AI is the true enabler of these services to market broadly and commercially, leading to a more regular income stream for firms, tremendous value-add for clients, and more interesting and impactful work for auditors.

…have better margins

Just like all compliance activities in the accounting industry, the annual compliance audit is considered a “grudge purchase” by many clients. They know they need it but don’t really like enduring the process or let alone paying for it. This puts huge downward pressure on fees and creates what is known as “margin-squeeze”.

With a combination of a more human, client-centric process (enabled and amplified by great technology), more value delivered through deep business insights, and the enablement of more valuable periodic services (for example), AI audit helps clients shift towards recognizing the opportunity for continuous improvement and peace-of-mind around quality that the audit process brings. This mindset shift is essential for audit teams to successfully position fees that reflect the value of the service delivered now and into the future, and thus preserve commercial margins for their firms.

AI auditing is here to stay

Just like Apple did with the release of the first iPhone and Xero did with the introduction of the single ledger, both in 2007, today’s AI auditing will reset client expectations for audit across the industry. Supremely efficient, deeply analytical, highly valued, and wonderfully human-centric audit experiences will re-define the audit process and profession and ultimately re-define the notion of reasonable assurance.

Want to learn more about how auditors are using AI?

MindBridge is proud to sponsor this year’s virtual Digital Accountancy Forum. The forum brings together leading accounting firms, industry bodies and regulators, advisors and consultancies, law firms, and tech vendors to discuss and challenge key issues impacting the sector.

On top of providing an opportunity to connect and network all day through the virtual booth, the event will also see MindBridge’s Founder and Chief Impact Officer, Solon Angel, present on how AI can help auditors keep companies out of trouble in a session at 3:00 pm BST.

Packed with valuable takeaways, the session will give real examples of how AI-based data analysis, planning, assertion testing and more can drive better client conversations and give auditors the evidence they need to back them up.

Solon adds: “From Carillion, to Patisserie Valerie, to Wirecard, the audit profession is being blamed for fraud schemes, scandals, and financial collapse. At the same time, the industry is slow to consider radically different ways of performing audit, and has instead focused on automation of the old ways of doing audit. It’s time to enable auditors to do their best, by giving them the knowledge and tools they need to uncover the truth behind an organization’s finances and visualize data in a way that empowers leaders to take action.”

But how can this be put into practice and how can AI really help?

Join Solon as he explains how machine learning works to augment human judgement, providing a clear understanding of how firms, regulators, standards bodies, schools and technology vendors can work together to restore trust in auditors.

At the end of the discussion, you will have heard:

Why AI offers much more than automation

How data science augments an auditor’s experience and judgement

How data analytics enables new ways of thinking and services for clients

Why restoring trust must include everyone, from regulators and firms to schools and technology companies

There will also be the opportunity to hear our Director of Growth Europe, Stuart Cobbe, join industry experts on the closing panel discussion. This session will explore the future of the accountancy profession, touching upon:

If globalisation will have an impact on developing the next generation of accountants

How the industry can ensure the accountancy profession remains attractive to the younger generation

What future technological changes are needed to increase the automation of accountancy

We look forward to seeing you there! Register your attendance here. You can also meet our UK and product teams at our virtual booth!

If you’re looking for tips on how to make the most out of attending a virtual event, take a look at these do’s and don’ts to get you started.

Yesterday saw the Digital Accountancy Forum return for the ninth year, but it was the first year our MindBridge team has been involved. The packed agenda, including a session from our Founder and Chief Impact Officer, Solon Angel and a panel discussion involving our Director of Growth Europe, Stuart Cobbe, was full of valuable insight celebrating the best and most innovative developments in modern accounting.

We were delighted to have many engaging conversations with delegates looking to find out more about MindBridge. In particular, our team spoke to numerous accounting professionals about the future of audit, what’s new in Ai Auditor, how AI can assess financial risk in times of crisis and why one of our customers, Moore Kingston Smith, a top 20 UK chartered accountancy and audit firm, is leveraging MindBridge’s Ai Auditor.

Introducing Ai Auditors

Solon’s session, discussing how AI can help auditors to keep companies out of trouble, was quite relevant in this Covid environment. Solon talked about what it takes to be an Ai Auditor, how data science can augment a human auditor’s experience and judgement, why data analytics and AI are slightly different, how they can enable new ways of thinking and why restoring trust must include everyone. It was a presentation packed with insight, takeaways and learnings for accountancy professionals.

Rounding up the session, Solon introduced the concept of Ai Auditors – human auditors that have been augmented with AI – with a great quote from Moore Kingston Smith about how working with MindBridge has enabled them to pick samples and look at different transactions in a more robust way:

“…if someone asks me why we have audited a particular sample, I can explain the computer-based technique which is a lot more robust than saying one of my trainees picked ten transactions…”

The future of accountancy firms

Towards the end of the day, MindBridge’s Director of Growth Europe, Stuart Cobbe took part in a panel session chaired by Jon Lisby, Director, Global Alliance Advisory Services, exploring where the accountancy profession is heading and what future opportunities might look like.

When discussing what the firm of 2025 will look like, Stuart added that accountants have been agile in their response to the pandemic, with a lot of changes underpinned by technology, enabling different ways to create and add value:

“The accounting or audit firm of the future will be more varied with its skill composition and it will be more agile in the way that it plans for its business. It will also be much more responsive to the needs of the market; less checklist-driven and more critical thought-driven.”

The new era of audit

We were thrilled with the volume of engaging and insightful conversations that our team had with delegates at the Digital Accountancy Forum. Commenting on the success of the event, Solon adds:

“The Digital Accountancy Forum was truly a great event, showing what can be achieved virtually! Every delegate we spoke to was keen to learn about Ai Auditors and how AI can really transform the audit process. We’d like to thank everyone who visited our virtual booth and attended our sessions – we’re already looking forward to next year’s event!”

If you didn’t get a chance to chat with one of our team members at the virtual booth but would like to find out more, please email info@mindbridge.ai.

In recent years, demand for accounting and audit software has been on the rise. Mostly, accounting professionals are looking for ways to speed up routine tasks and focus on what matters most—providing clients with valuable business insights and guidance on financial strategy. Already, many firms have seen how AI audit software can help their teams improve risk assessments and build stronger audit plans. That’s because some of the best audit software helps auditors become more efficient at combing through surging amounts of company data.

As we move through 2021 and into 2022, the interest in AI audit software isn’t slowing down. Below, we’ve identified five key trends that we believe will continue to propel the accounting and auditing industry forward in adopting AI audit software.

5 audit software trends to keep an eye on:

1. Increased demands for automating routine tasks

Accountants and auditors are under a lot of pressure to identify risks and turn reports over in the least amount of time.

The challenge is that when auditors use traditional data sampling and analysis methods, billable hours can add up fast. This is why in recent years there has been a push for greater automation in accounting practices using audit software. Some of the best audit software combines machine learning, data analytics, and AI to deliver higher levels of automation on routine tasks.

By automating processes with AI audit software, auditors can reduce the off-chance of human error while also ensuring 100% of the data is thoroughly analyzed for risks. This frees up an auditor’s time to focus other critical tasks such as exploring data trends and studying risks characteristics so they can ultimately deliver greater value to clients. As we move into 2022, these tangible efficiency gains will continue to drive the adoption of AI audit software.

2. Growing adoption of cloud-based solutions

In recent years, cloud-based software has become increasingly popular in the accounting and finance industries. Since these cloud applications are hosted in highly-secure remote datacenters, it’s easier for accountants to access information from home offices. They simply login to an online platform which is protected with built-in cybersecurity features.

If we look at statistics from 2018, about 43% of CPA firms already had employees regularly working from home. And according to Accounting Today, the global spread of COVID-19 has already contributed to a sudden surge of businesses moving over to cloud-based bookkeeping software.

Even before COVID-19, a survey conducted by Sage reported that about 67% of accountants believed that cloud technology can make their roles easier. And 53% of the respondents had already adopted cloud-based solutions for project management and client communication.

Near the end of 2021, we expect that this trend toward enabling remote work with cloud-based solutions will significantly increase for accounting and audit software as well.

The ability to thoroughly mine the entirety of a company’s financial data requires smart tools. AI audit software helps auditors go through and make sense of large volumes of data in very little time. As touched on earlier, this increases an auditing team’s productivity and allows them to generate more accurate insights for the client.

For 2021 fiscal year-end audits, auditors are in a unique position to tackle these risks head on using AI audit software. That’s because the audit software enables better fraud detection and risk assessment by testing and performing statistical analyses on 100% of a company’s financial data. With a higher likelihood of fraud looming this year, accountants could be more willing to put AI software to the test.

Traditionally, financial statement audits were driven by statistical sampling of past activities. But auditing practices as we know them are changing quickly. With access to more automated solutions, the future of auditing will likely involve real-time transaction analysis, risk evaluation, and data validation.

As we look ahead, auditors will likely be spending less time handling those manual, time-consuming audit procedures in 2022. Instead, auditing teams will have an opportunity to shift resources towards analyzing data, providing insights, and advising their clients. According to experts, a hybrid approach that combines the use of accounting technology and a focus on financial advisor input will continue to gain traction in the near future.

It’s time to capitalize on AI audit technology

While we can’t predict the future, we do know this— AI audit software will continue to help accountants and auditors gain deeper insights into their client’s financial data, in less time. Overall, the audit software can increase the efficiency of their processes, so they can focus on delivering better results. Those who are forward-thinking and ready to embrace artificial intelligence and audit technology will reap great benefits today, and tomorrow.

Artificial intelligence (AI) and machine learning (ML) technologies can streamline traditional audit procedures for Accounts Receivable (AR) and Accounts Payable (AP) in audits of financial statements.

This blog will consider applications of AI and ML technologies using the MindBridge platform for both substantive analytical procedures as well as detailed testing of specific items.

What does the MindBridge platform do?

MindBridge Ai Auditor, in addition to core general ledger analysis, includes dedicated AR and AP modules that automatically analyze subledger data and, without any scripting, provide high-value visualizations and transaction-level analysis of data.

These capabilities allow you to leverage subledger-level insights and anomalies as critical inputs to your audit procedures and identify risks of material misstatement.

How MindBridge empowers you to perform effective and substantive analytical procedures for AR and AP

Substantive analytical procedures can be a powerful complement to traditional sampling and external confirmations. That is, provided that the auditor is comfortable with the internal controls in place regarding purchasing and sales cycles and has validated the accuracy and completeness of the subledger data.

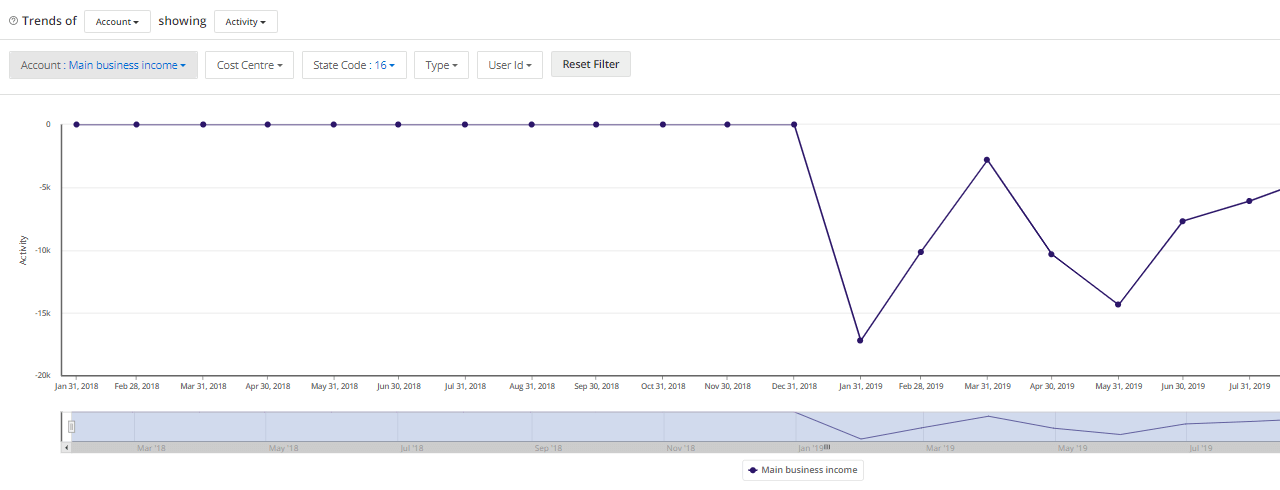

Trends and patterns

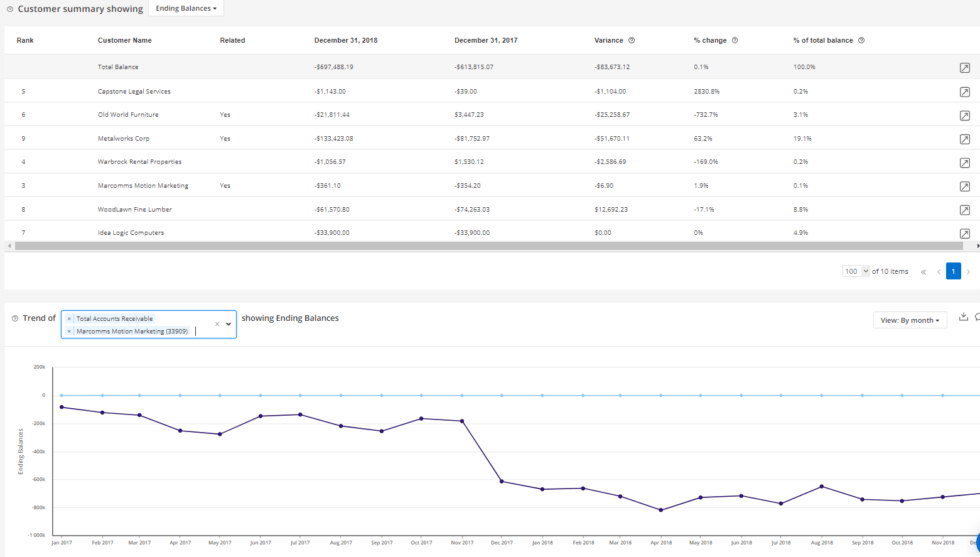

Ai Auditor allows you to visualize how monthly AR and AP balances or net monthly activity track over multiple years at customer vendor levels, and in aggregate. Consistent patterns in these trends in the face of consistent sales and purchasing patterns (respectively) may provide audit evidence that subledger information is not materially misstated.

Vendors and customers related to the entity subject to audit are flagged directly in the summary detail as well.

Key performance indicators

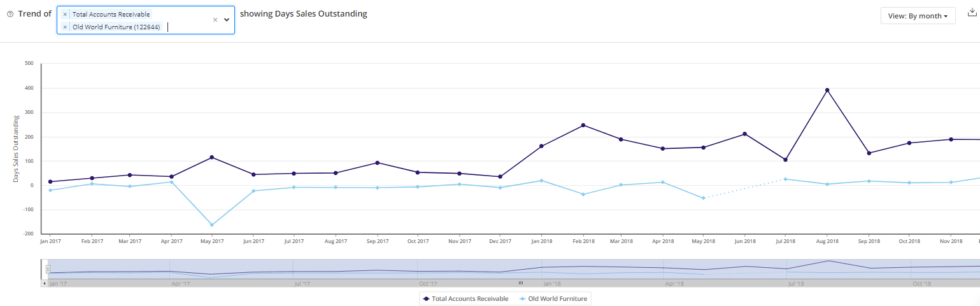

Days Outstanding and Turnover Ratios are calculated at the customer and vendor level and are visualized on a monthly basis, allowing you to identify where there are periods of potential distress or deteriorating quality (e.g. is the volume of cash receipts slowing?). Similar to ending balances and activity, you are also able to compare certain customers or vendors against each other along the lines of these metrics to expose patterns of interest.

Aging

Aging at the customer and vendor level is automatically calculated and captured across respective buckets of days outstanding (0-30 days, 31-60 days, etc.). Consistent breakdown in the relative proportion of these aging buckets across multiple years of subledgers may provide audit evidence that subledger information is not materially misstated at the balance sheet date.

For certain entries that are significantly aged or stale, you’re able to drill-in to all the transactions with a particular customer or vendor and ascertain which invoice(s) are contributing to those totals and whether they could be at risk of bad debt.

How MindBridge streamlines detailed testing of AR & AP subledger data

Navigating and querying transactional level data via the Data Table in Ai Auditor is a powerful and effective way to explore and validate subledger activity.

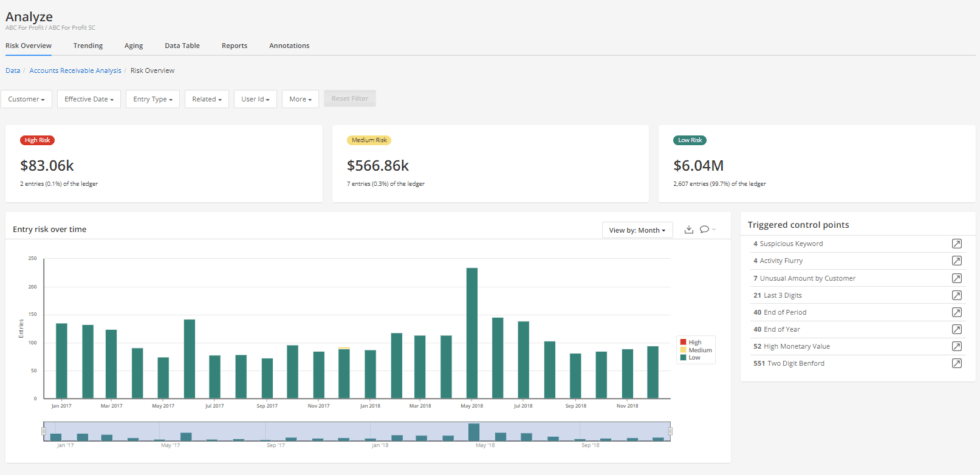

Control Points, which are various statistical, rules-based, and machine learning tests, are run against every transaction. The results are summarized on a dashboard that supports interactions like filtering and drill-through.

Combining the query building capabilities of the Data Table with Control Point tests, you can efficiently identify relevant populations for sampling and have selections for external confirmation requests or alternative procedures testing (like subsequent receipts, for example) automatically identified on a risk-stratified basis. These selections can then be exported to Excel in one click to populate confirmation requests and/or to be included in supporting documentation.

The results of the transactional risk analysis may also be of particular interest to large entities and small businesses alike to provide insight into where there may be process improvements or gaps to consider in internal controls.

Take the first step towards AI-driven audit procedures on the AR and AP subledgers

Internet companies have been driven by data for decades. For instance, Amazon was using basic AI systems over 20 years ago. Netflix, Microsoft, Google and many others have dominated their categories by using a data and algorithms-first approach. Yet when we look at the accounting world, many still believe that data and analytics are a novelty, optional, or separate from the work that they do.

When it comes specifically to journal entry testing, most auditors today have been using antiquated approaches and sampling techniques. Many justify the use of these limited audit risk methods by saying they comply with existing standards. But these standards such as SAS 99, Consideration of Fraud, actually only require auditors to gain an understanding of the business and focus on identifying items that warrant further auditor considerations.

According to SAS 99 or other international standards, there is nothing to discredit the use of advanced methodology and latest AI-powered technologies. In fact, almost 20 years ago, the American Institute of CPAs published the 2003-02 Practice Alert with guidance for the use of analytics. Today, recent advancements in auditing software allow accountants to better evaluate audit risks and deliver pertinent insights to various stakeholders.

The challenges with traditional journal entry testing

Traditionally, accountants had a lot of groundwork to do during an audit risk assessment. First, they would spend a considerable amount of time doing data preparation on usually limited data columns and file sizes. Then, they would try to determine which analytics to apply to the data.

As Enterprise resource planning (ERP) systems grow more complex, not all audit procedures can keep up. Data clipping or manually converting a GL report into an Excel file is known to exclude data or cause errors during the audit process.

Existing script-based data analytics engines are exclusionary based, meaning they extract data as an auditor applies various procedures. This decreases the chance of detecting anomalies and doesn’t allow for a truly comprehensive audit risk assessment. This is why many leading accounting firms, including the Big Four, are moving away from these outdated auditing procedures. These more traditional methods for risk-based journal entry testing cause inherent liability and poor quality.

Using more advanced AI-powered auditing software, an audit team can gain more far-reaching insight. By pinpointing control points, the AI auditing software can identify and learn what’s normal or not and then analyze a wider range of data without inherent exclusions.

3 ways to automate risk-based journal entry testing

1. Start with a data-first approach

Before thinking about which audit tests or procedures to apply, you need to start with the data. This is called a bottom-up approach to audit risk assessment, instead of top-down. The idea is to let the data speak first. Then, you can look for standard procedures and identify any underlying risks.

Seek to get as much information on the system available as possible from your client: GL reports, Charts of Accounts, opening and closing balances, bank statements, as well as the previous year’s data.

With this modern approach, you can leverage historical data in new ways. This can include automatically doing pre-emptive calculations and forecasts to better understand potential audit risks.

For example, MindBridge Ai Auditor automatically generates ratios and forecasts that you can annotate and add to your audit plan, seamlessly.

2. Leverage the community effect

Try to avoid reinventing the wheel and be curious of what automation can accomplish. It is not just about using new auditing technology. Try to understand the definition of risk that is built into the automation. A few AI or cloud accounting software vendors like MindBridge have spent countless hours with industry partners embedding specific risk analysis into their software packages.

Auditors are required to “test the appropriateness of journal entries recorded in the general ledger and other adjustments”. In the past, you would have had to define the procedures yourself. But today, with everyone connected online, communities have emerged around your choice of tools. These communities include other accountants that might have implemented fully automated procedures into their methodology and are eager to contribute best practices and tips with others.

Your clients are not in the business of ensuring the right controls or worrying about anything else other than running their business. They simply don’t anticipate bad behavior, bad actors, or white-collar criminals. It is not enough to just design procedures or automate the classic CAATs-style audit tests. Instead, you can leverage the full power of advanced audit risk assessment techniques such as “Rare Flows” and “Expert score” using powerful AI auditing software. These improve your ability to detect high-risk transactions or the sidestepping of the company’s internal controls.

Some employees, including senior management learn ways to work around a specific control. For example, employees can post numerous smaller journal entries to various departmental general ledgers to circumvent approval processes. This also makes it more difficult for auditors to detect the fraud.

This is where AI can excel and really help you. Rare flows and unusual transaction analysis can help you quickly identify audit risks and conduct a more thorough journal entry testing. After saving time on the previous tasks, you will be able to dig into the data and ask the right questions.

Evolving audit risk assessments and your business

Accountants and auditors are not here just to perform repetitive tasks or follow outdated procedures. The core principle of the profession is to be business advisors to their clients.

By using advanced technology for risk-based journal entry testing, auditors can streamline the auditing process and avoid spending billable hours digging for issues in only one area. Instead of limiting themselves to simply extracting data from a general ledger, they can ask for more reports and more data. This allows them to get a deeper understanding of all the anomalies in client files to perform a more thorough audit risk assessment.

A new audit evidence standard has been released by the American Institute of Certified Public Accountants (AICPA) that includes significant updates around how technology and automation can be leveraged throughout the audit process. Here, we’ll examine this standard and some of the most significant examples of how the AICPA has explicitly considered the applicability of analytics and automation to how audit evidence is gathered and concluded upon.

While the effective date of the guidance allows for lead time for the appropriate methodology changes and technology investment to be contemplated and implemented by firms ahead of calendar 2022 audits, the updates reflect the massive tailwinds of how data analytics and automated tools and techniques are well-positioned as catalysts for the reimagining of the audit life cycle. Furthermore, the potential afforded by these technologies to drive monumental improvements in both quality and effectiveness is only amplified further in today’s remote work environment.

Key concepts around audit evidence

It’s worth revisiting some of the basic principles around audit evidence and the responsibilities of the auditor before discussing how data analytics and automation can be transformative to how evidence is collected and generated.

The new standard clearly defines the auditor’s objective around audit evidence as follows:

“The objective of the auditor is to evaluate information to be used as audit evidence, including the results of audit procedures, to inform the auditor’s overall conclusion about whether sufficient appropriate audit evidence has been obtained.” (SAS No. 142, par 5)

The term audit evidence may conjure up images of stacks of source documents (invoices, purchase orders, cheque stubs, etc.) and detailed documentation of ticking and tying them all together in an Excel spreadsheet. But audit evidence isn’t just the outcome of detailed transaction-level testing, it’s more broad and includes the results of your risk assessment procedures and inquiry, any testing of controls, and the results of both detailed and analytical-based substantive testing (SAS-142, par A44).

In other words, the auditor, in exercising their professional judgement as to whether identified risks are properly responded to, has a wide net of support to consider on balance and weighed together to make that conclusion effectively.

So what type of things influence whether evidence is sufficient and appropriate? This comes down to how much evidence is required to respond to the identified risks of material misstatement, and how relevant and reliable that evidence is. The appendix to the standard specifically includes a number of examples and contemplation of what these key terms mean in practice and some of our takeaways (not exhaustive) include:

What types of factors impact the reliability of audit evidence?

Source

Is the information from an external source, and therefore less susceptible to management bias (SAS-142, par A22)?

Nature

Is the evidence “documentary” vs. provided orally through inquiry?

The controls over the information and how it’s produced

How automated is the process by which data is generated and what is the relative strength of controls that the entity has in place? How is the accuracy and completeness of the information ensured?

Authenticity

Has a specialist been involved in validating certain assumptions?

What types of factors impact the relevance of audit evidence?

The accounts and assertions it relates to

Does the evidence tie directly to identified risks at the assertion level of an account? For example, purchase documents matched to payable transactions right before balance sheet date provides evidence against an early-cutoff risk but not a late-cutoff risk.

The time period it pertains to

Does the evidence relate to the period under audit or specific subsets of that period where risk is relevant?

Susceptibility to bias

How much influence over the information does management have?

These concepts are critical to keep top of mind as we consider the role of data analytics and automation because introducing technology to the audit process doesn’t diminish the auditor’s overall objective and requirement to obtain sufficient and appropriate evidence to support their opinion. Rather, the tests and techniques that we’ll review enable the auditor to more efficiently gather, interpret, and perhaps even generate the evidence that satisfy these criteria.

Facilitating high-quality and data-rich analytical procedures and risk assessment

Let’s consider the following excerpt from the new standard:

A59. Analytical procedures consist of evaluations of financial information through analysis of plausible relationships among both financial and nonfinancial data. Analytical procedures also encompass investigation as necessary of identified fluctuations or relationships that are inconsistent with other relevant information or that differ from expected values by a significant amount. Audit data analytics are techniques that the auditor may use to perform risk assessment procedures…

A60. Use of audit data analytics may enable auditors to identify areas that might represent specific risks relevant to the audit, including the existence of unusual transactions and events, and amounts, ratios, and trends that warrant investigation. An analytical procedure performed using audit data analytics may be used to produce a visualization of transactional detail to assist the auditor in performing risk assessment procedures….

Automated techniques such as the ones described in the guidance can be a very powerful and efficient method to assess relationships across the financial ledger. Having this type of analysis “out-of-the-box” at your fingertips, without detailed scripting or manual data wrangling, promotes efficiencies as well.

Here are a few examples of how the capabilities of MindBridge Ai Auditor align with a technology and data-driven analytical review and risk assessment that the standard explains.

Trend analysis

Our Trending analysis allows you to visually compare how one or more accounts moves over time. This allows you to assess how accounts or financial statement areas that you expect to be correlated (accounts receivable and revenue, revenue and costs of sales, etc.) are indeed tracking consistently. It’s important to note that this analysis is available on a monthly basis and is not just a simple year-over-year comparison. This empowers you to have a more nuanced view of what these relationships look like seasonally and more broadly.

You are also able to layer in filtering of the trends you are seeing, across additional operational dimensions of the financial ledger. For example, if an organization manages it’s P&L by department or region, you can examine how revenue breaks down across one or more of these dimensions with one click.

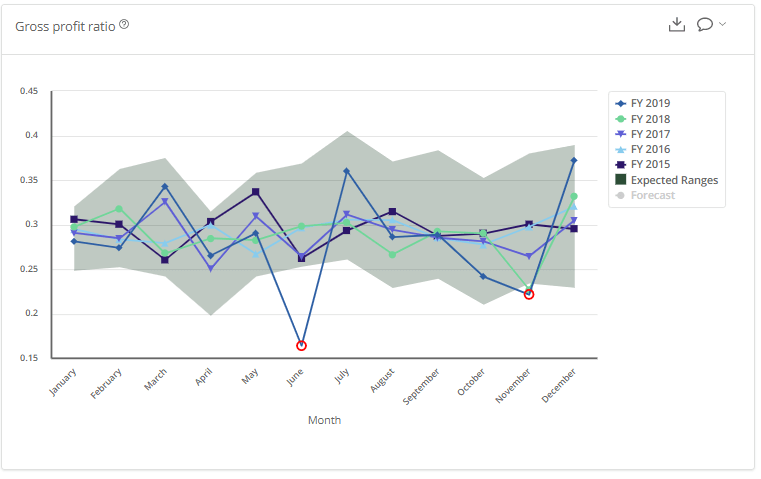

Ratios

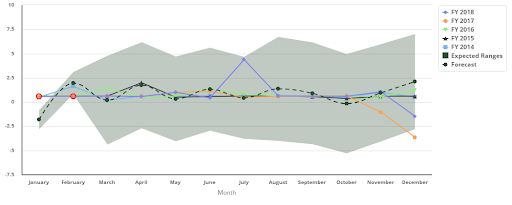

Over 30 critical ratios are automatically calculated by Ai Auditor and the results are visualized on a monthly basis throughout the audit period. How each ratio trends in the current period against prior periods is readily apparent and points of deviation can be flagged for further investigation with your client.

With an appropriate amount of prior period data available, Ai Auditor performs a regression analysis called seasonal autoregressive integrated moving average (SARIMA) to graphically visualize the expected ranges for the ratio in the current period in addition to the trend lines. This is extremely valuable in identifying algorithmic outliers for further audit procedures and input to risk assessment.

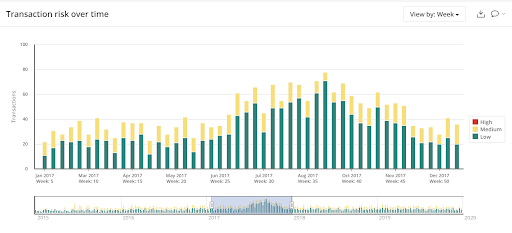

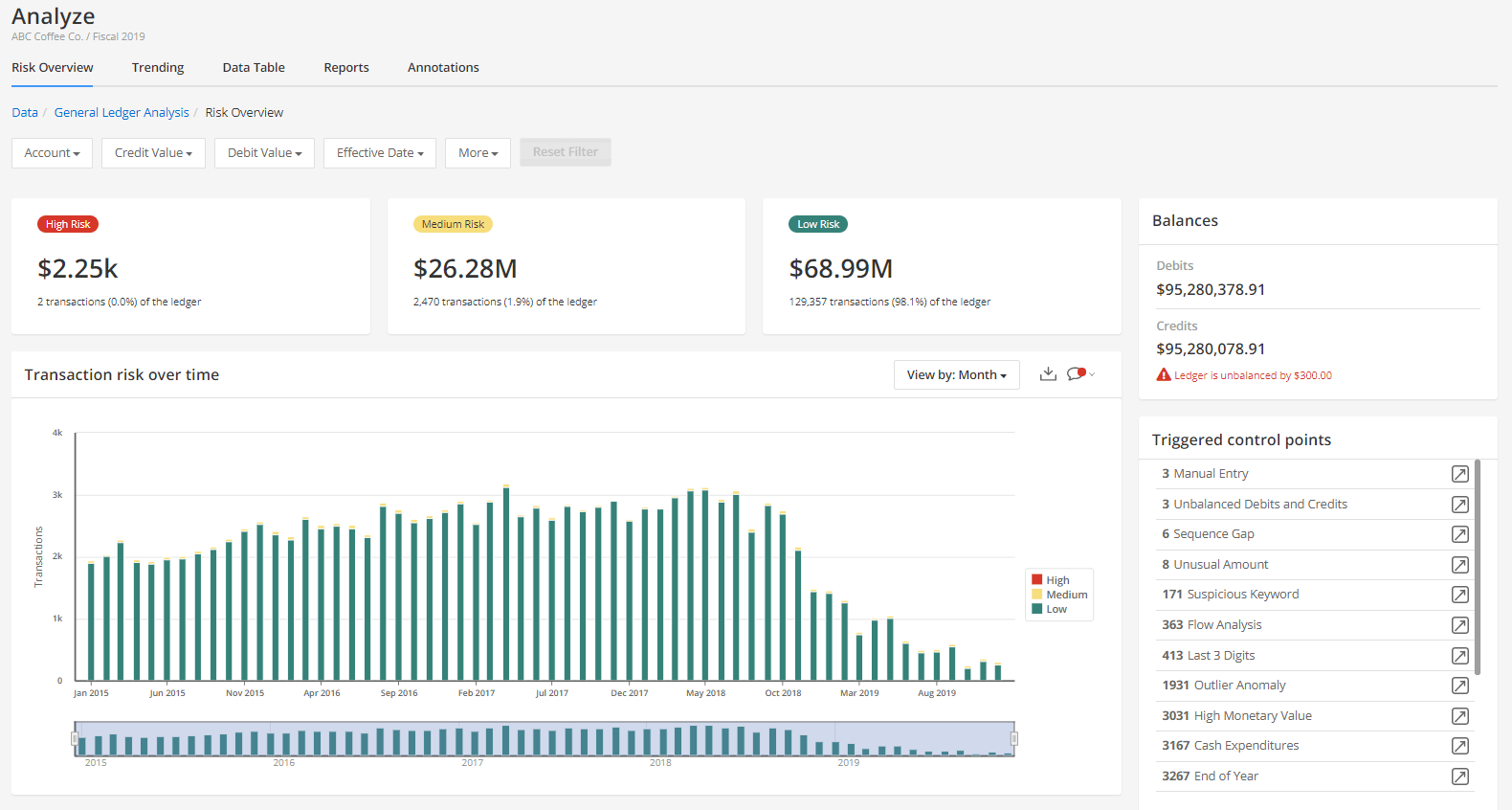

Transaction-level analysis

The new standard specifically contemplates how unusual transactions or events in the financial ledger impact risk assessment and this aligns perfectly with Ai Auditor’s core competency of an ensemble-based AI algorithm that runs against every transaction and tags it with a single risk score:

A61. Analytical procedures involve the auditor’s exercise of professional judgment and may be performed manually or by using automated tools and techniques. For example, the auditor may manually scan data to identify significant or unusual items to test, which may include the identification of unusual individual items within account balances or other data through the reading or analysis of entries in transaction listings, subsidiary ledgers, general ledger control accounts, adjusting entries, suspense accounts, reconciliations, and other detailed reports for indications of misstatements that have occurred. The auditor also might use automated tools and techniques to scan an entire population of transactions and identify those transactions meeting the auditor’s criteria for a transaction being unusual…

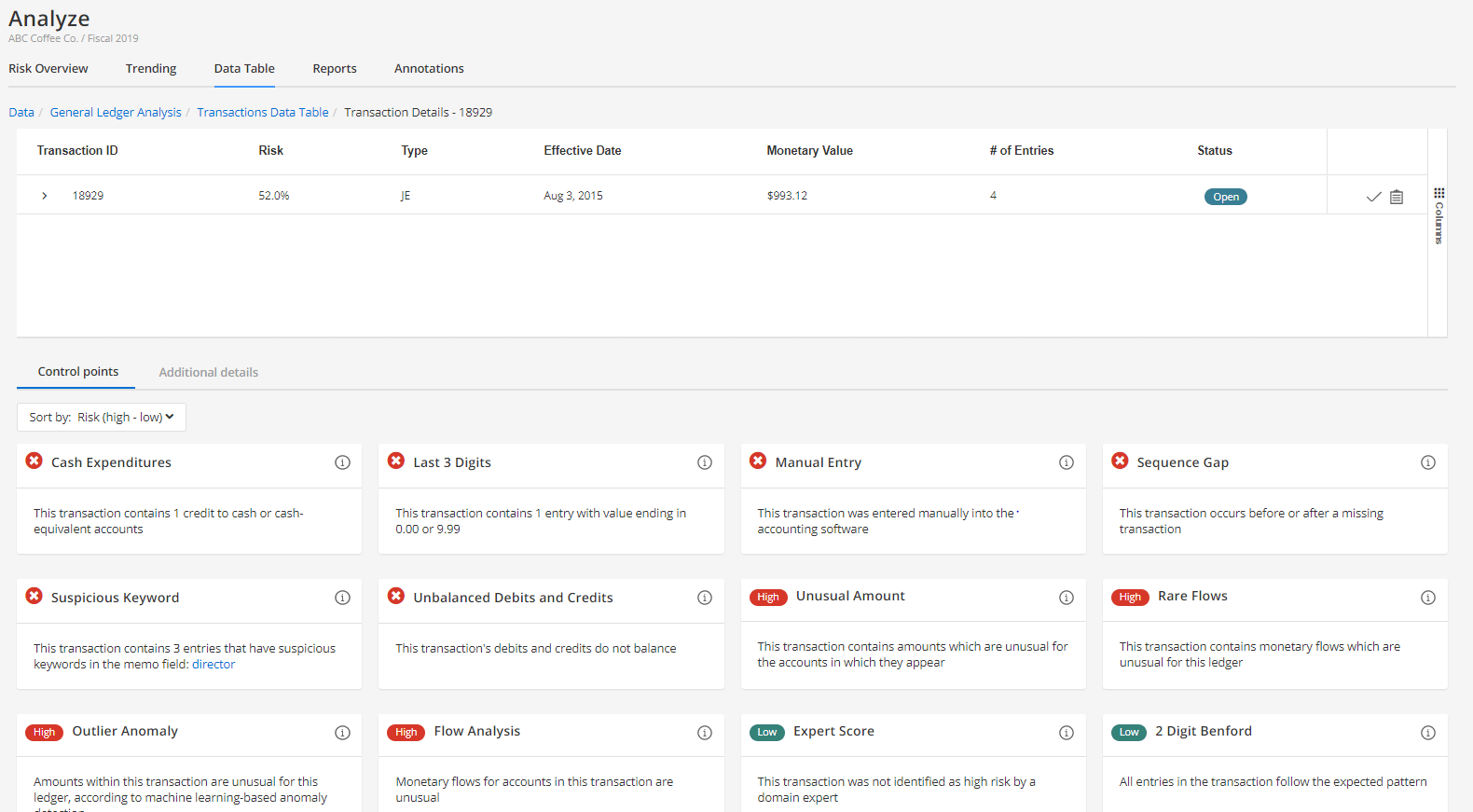

In Ai Auditor, the ensemble-based algorithm includes over 30 different tests, termed Control Points, which range across rules-based, statistical methods, and machine learning-based techniques. The ensemble specifically includes tests for Unusual Amounts posted to an account, Rare Flows of money between accounts that don’t normally interact, and Outlier Anomalies.

With Ai Auditor, you can visualize the results of these tests in aggregate via dashboarding and drill down to the most granular level of a particular entry to see which Control Points are contributing to a certain score.

Techniques that facilitate highly efficient “dual-purpose” procedures

The new standard includes an illustrative example where a series of audit data analytical techniques are used as both a risk assessment procedure and a substantive procedure:

A46. An auditor may use automated tools and techniques to perform both a risk assessment procedure and a substantive procedure concurrently. As illustrated by the concepts in exhibit A, a properly designed audit data analytic may be used to perform risk assessment procedures and may also provide sufficient appropriate audit evidence to address a risk of material misstatement.

The exhibit being referred to in the passage above is quite compelling and certainly worth a detailed review (beginning at page 42 here). As an extension of the previous discussion around transaction-level risk scoring, assuming that additional considerations are satisfied, such as the effectiveness of controls over how the information is produced and the auditor’s confidence as to the accuracy and completeness of the information, the ability to “profile” transactions into relative risk buckets using an audit data analytic (ADA) routine is explicitly contemplated here.

If the results of that “profiling” can be used to not only to inform risk but also the nature, timing, and extent of further substantive audit procedures, the investment into building and integrating these types of techniques into your methodology could provide significant ROI in terms of execution efficiencies.

Take the first step towards a modern, data-driven technological approach to audit, contact sales@mindbridge.ai.

Three ways Ai Auditor strengthens your audit planning

The determination of where audit risks of material misstatement lie is a critical output of the audit planning process. Usually, identifying those risks is based on the auditors understanding of their client and the client’s operating environment. Auditors can now rely on a data-driven approach to better understand that environment. And this will positively impact the nature, timing, and extent of the audit procedures which respond to the identified risks.

How to enhance your audit planning using Ai Auditor:

1. Conduct thorough assessments for better audit planning

Just looking at a balance sheet or income statement at one point in time isn’t enough. Analyzing more financial data during the planning phase allows for a deeper understanding of the client’s operations.

Auditors have long used analytics to help assess a client’s operations. These tools help them gain insights and identify aspects of the entity that were either unknown or unfamiliar to the auditors. These data analytics essentially help them to better assess the risk of material misstatement, as well as provide a basis for designing and implementing responses to the assessed risk.

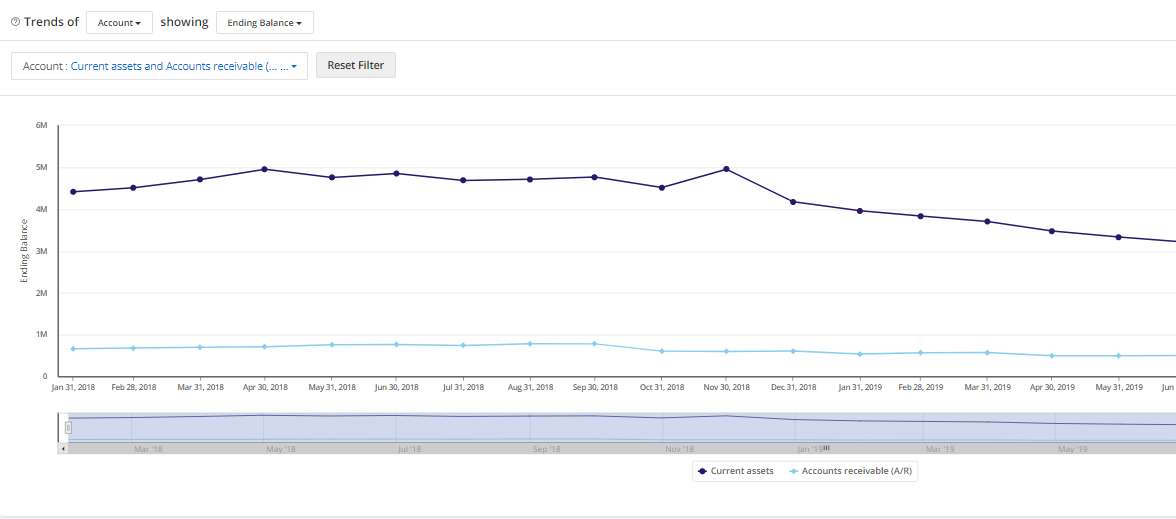

Working with Ai Auditor, the auditor can select a view of the ending balance or monthly activity. They can also analyze different transactional relationships within the general ledger to ask better questions and make more precise judgement calls.

For example, let’s say an auditor finds out the accounts receivable (AR) has a 10% change from the prior year to this year. The auditor can explore the AR activity and find out if this change was a normal increase or if there was any unusual activity that could indicate a new large customer or purchase at year end.

Another example would be if there was an account that had no significant change from the prior year ending numbers, but the activity was much different. Having more data would provide the auditor with better insight into the client’s operations.

Using Ai Auditor, an audit team can also look at relationships between accounts to identify if there are any unusual patterns. For example, perhaps they’ll notice that the cost of goods sold (COGS) and inventory trends appear to not follow consistent patterns. The auditor can then include a very specific and strategic task in the audit plan — to pinpoint the time when the trend does not follow expectations and investigate further.

2. Quickly identify unusual transactions across all data

The machine learning engine in Ai Auditor looks at each unique data set and analyzes the frequency and amounts of the transaction. The engine also explores relationships between the account’s transactions that are being recorded.

Ai Auditor helps automate the analysis by flagging items that just don’t fit typical transaction patterns. It’s then up to the accountant to focus on the most uncommon and unusual items and dig deeper.

For example, Ai Auditor might flag the write-off of inventory because insurance-related payments seem uncommon or unusual. During the audit, the auditor might learn that this was due to a warehouse fire.

Essentially, the platform gives auditors better visibility on these unique circumstances right from the start of the audit. The auditor can then focus on these higher risk transactions, consider the ramifications of the transactions, and understand how those riskier items might impact the financial statements.

3. Retrieve and view transactional breakdown by audit area

Using Ai Auditor, an accountant can filter risks by category. This allows them to breakdown risk by account, branch, program, type of transaction, time, monetary value and more.

With this breakdown, the auditor will gain a better understanding of where relative risk lies across operations. They will also be able to see which control points are being triggered within a specific area and consider how that impacts the overall audit risk.

For example, let’s assume an auditor notices that the accounts payable (AP) entries are triggering a significant amount of risky transactions at year end, specifically in the Southwest branch of the operations. This might indicate cutoff issues. Or, if the sequence gap control point is triggered, perhaps the auditor will assume there are completeness issues.

During audit planning, auditors who think critically about how these control points might factor into the assertions for the various accounts will drive stronger results.

Using the AI auditing platform, accountants can then uncover valuable insights to supplement their discussions with management and existing knowledge of the client. Those insights might include uncommon patterns in transactions, abnormal stratifications, unusual relationships between accounts, and breakdowns of trends or ratios. With this information at hand, auditors can ensure a well-planned and successful audit.

Accounting software trends have impacted the accounting profession in big ways. And in my view, one of the greatest analogies of this impact, and even of the way our team at MindBridge delivers value to our clients, comes from Sam Daish, Head of AI and Data Science at Qrious.

A story of three types of businesses

In his previous role as General Manager of Data Innovation at Xero, Sam addressed a room full of very traditional big-firm accounting partners. During this talk, he described the evolution of manufacturing in the time when electricity was new. He summarized the journeys of three business types:

Those who thought electricity was some strange wizardry and continued on as they always had

Those who tried to adapt their processes around electricity to make things work

Brand new businesses that sprung up native to electricity

Sam continued to tell the story of how manufacturing evolved in the 1880s. Businesses in the first category simply could not compete. They buried their heads in the sand. Their refusal to adapt was largely due to long-held pride in traditional expertise. The second group worked really hard to re-invent efficient processes—to make electricity bend and work around the way they’d always done things. The third set of businesses built operations with electricity at the heart. What happened to them?

The ‘ostriches’ were completely obliterated by the rest of the market

The ‘adapters’ really tried, but many businesses did not survive

The ‘electricity natives’ absolutely consumed the market. They shifted customer expectations and quickly devoured customer relationships that were long-held by large, big-brand traditional businesses that once dominated the industry

The parallels with the accounting industry’s state of flux surrounding technology adoption are profound.

First comes cloud accounting software, then AI accounting software

At one point, there was so much fear, worry, and apprehension about cloud accounting software. Many believed the accounting software would steal jobs from bookkeepers, graduates, and accountants in general. Yet the only ones who have experienced any negative outcome have been those who failed to adopt and adapt. Accounting firms who have embraced cloud accounting software and the client-centricity of the single ledger, and who have assisted their clients in doing the same, are dominating the market. It is not accounting technology replacing accountants – it’s accountants adopting technology that are replacing those accountants who are not.

So what about AI now?

Most would agree that diversification into advisory services is the key to modernizing accounting firms and aligning with client expectations. During Covid-19 times, we have seen a reversion back to the bread-and-butter of compliance for many accountants. What we will see moving forward is the evolution of compliance; it will feel less like putting numbers in a box and filling out forms (as this becomes more and more automated over time) and more like compliance risk mitigation, or ‘compliance advisory’. So for the future-fit compliance and advisory firm, AI accounting software comes to the fore when we ask ourselves: “So you have access to all this real-time data via cloud—what are you doing with it?”

When we look at accounting software trends, the message to support the adoption of AI is like that of cloud: “AI—it’s about task replacement, not human replacement”. The automation and ‘task replacement’ we now enjoy with cloud accounting software is similar to AI accounting software—these technologies are just doing parts of the job which no one likes anyway. For example, we love presenting insights to clients, showcasing our deep expertise of industry, and offering fancy visualizations that break down the complex into a simple picture. But we don’t like entering or churning through the data to get to the insights. So for this, we have AI. In a recent Accounting Today article titled ‘What AI does for accountants’, the author describes three areas in which accountants can leverage AI accounting technology right now:

Invisible accounting to automate reconciliations for clean, timely data

Active insight to drive better decisions

Continuous audit to build trust through better financial protection and control

Stepping towards success with AI

No matter where accounting firms are in their journey towards adopting new accounting software, one thing is clear—businesses need to, at the very least, start looking at the latest advancements in AI and all the advantages it offers, or risk being left behind. Some may be just jumping onto the cloud accounting software train. Others may begin courageously diving into AI. Regardless, there is a necessity for our established industry of accounting professionals to be deliberate about their re-learning journeys when it comes to accounting software. Those who seek to not only survive, but thrive, must ensure that data literacy and conceptual knowledge of what both cloud and AI accounting software can deliver are key to their business strategy moving forward.

An effective audit starts with a solid audit plan. While the overall audit strategy and plan can vary between clients, an auditor will usually establish risk assessment procedures and a how-to response for the risk of material misstatement.

The challenge is that sometimes, even the most thorough and comprehensive audit plans can still have gaps. In fact, every auditor understands there will likely always be some degree of uncertainty and unidentified risks before an audit begins. It’s in the initial audit planning stages that an audit team will often ask:

How can we lessen those unknown risks?

Is there an opportunity to confirm initial assessments about the industry or company?

Are there blind spots that we haven’t considered?

This is where machine learning (ML) and artificial intelligence (AI) can help. In this blog, you’ll learn how you can use MindBridge AI to spot risks and shift resources during preliminary engagement activities through each phase of the audit planning process.

Pinpointing audit risks using a data-driven method

Identifying the inherent business risks associated with the company is an important first step in the audit planning process. An auditor must analyze key risk factors such as understanding the industry risks, the company’s business, and any recent changes within the company to determine if and how these considerations will impact the audit plan.

Using Ai Auditor, an audit team can enhance the risk assessment process by retrieving powerful risk insights. That’s because Ai Auditor examines 100% of the company’s transaction data and alerts the team to any anomalies or underlying risks associated with the entity. With detailed data at-hand, the audit team can then move forward with greater confidence in the audit engagement, trusting that the risk assessment is comprehensive and complete.

Ai Auditor can also help the team to identify new risk areas that have might not been flagged in previous audits and include them in their audit plan. Not only does this ensure a well-planned audit, but it also minimizes the potential for duplicating audit procedures later on.

Evaluating the effectiveness of the company’s internal control over financial reporting is another area where using Ai Auditor can be a benefit. Much like traditional testing, the platform automatically identifies control points to spot high-risks transaction data. The auditing team can also adjust these control points and use other capabilities within the platform to recreate traditional control testing models. This data-driven audit method saves the team time while ensuring high levels of accuracy and diligence.

Building an effective audit strategy with Ai Auditor

After initial risk assessments and tests, the auditors will be able to establish an overall audit strategy. This sets the scope, timing, and direction of the audit and guides the development of the audit plan.

For instance, the audit team will derive important conclusions after evaluating the effectiveness of internal control over financial reporting. These will help them decide whether to use control testing, substantive testing, or a combination of both in their audit plan.

When planning the timing of the audit, the team might also consider using Ai Auditor during interim analysis and take advantage of roll-forward capabilities at year-end to ensure a more effective audit.

Considering how much time and resources go into an audit, Ai Auditor can become a force-multiplier for an audit team. The platform provides insights that help them become more efficient as they move through audit planning to engagement completion.

Developing an audit plan with data at your fingertips

As an auditor begins developing and documenting the audit plan, the reporting features within Ai Auditor can help. An auditing team can export powerful graphs and data to support the audit plan regarding details such as the planned nature, timing, and extent of the risk assessment procedures; the planned nature, timing, and extent of tests of controls and substantive procedures; and other planned audit procedures.

The team can also use Ai Auditor to download a single report that details any flagged items and automatically add this report to the audit plan. This ensures the team conducts deeper investigations on those transactions or simply helps to justify why certain samples were selected.

Completing the audit engagement with success

Ai Auditor helps to simplify auditing planning. The platform offers valuable insights and data that help an auditing team streamline risk assessments, build an effective strategy, and outline a comprehensive audit plan. And since an audit team will be able to conduct investigations easier and faster through every phase of the plan’s process, they’ll have more time to offer clients valuable insights and guidance.