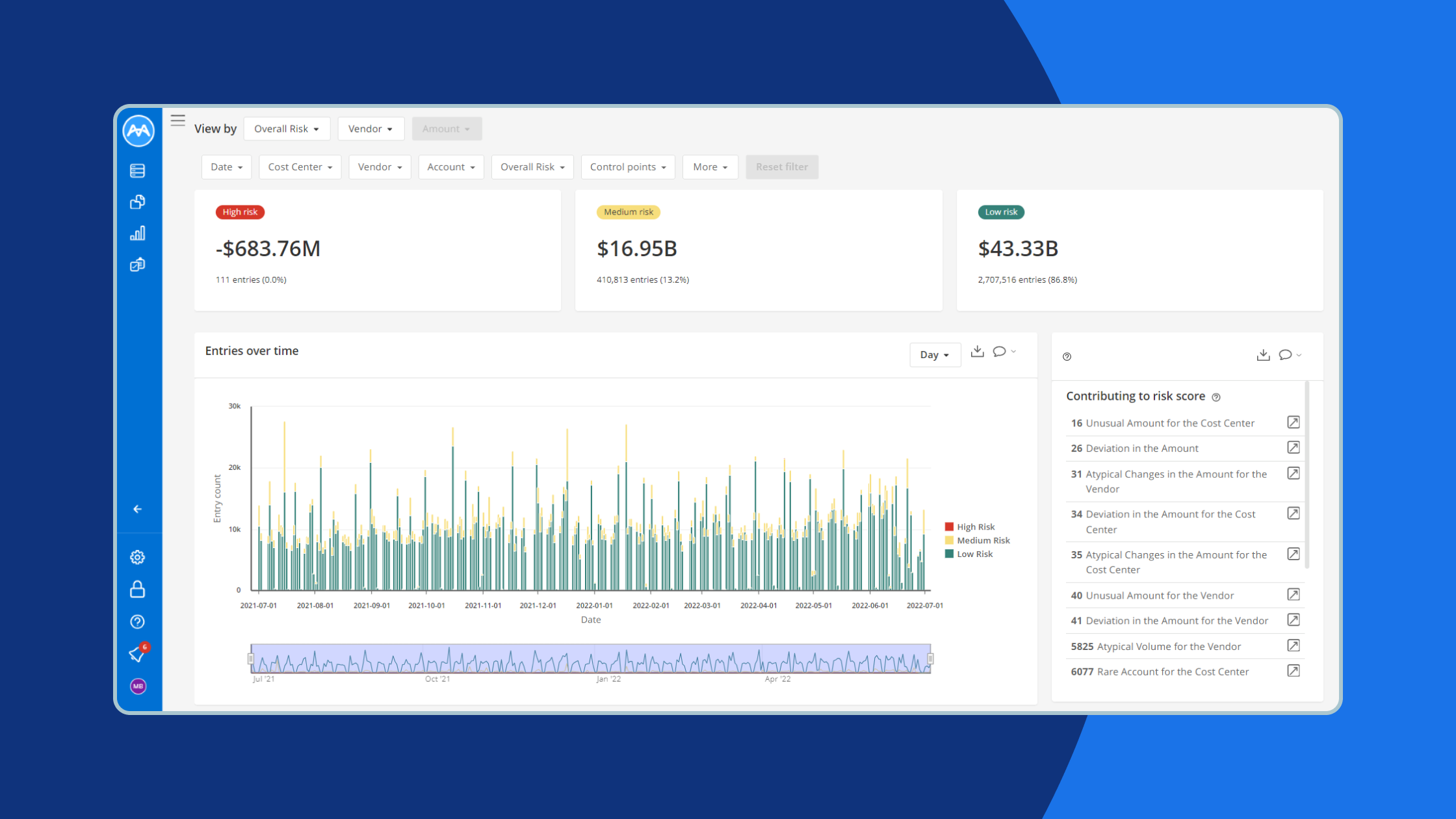

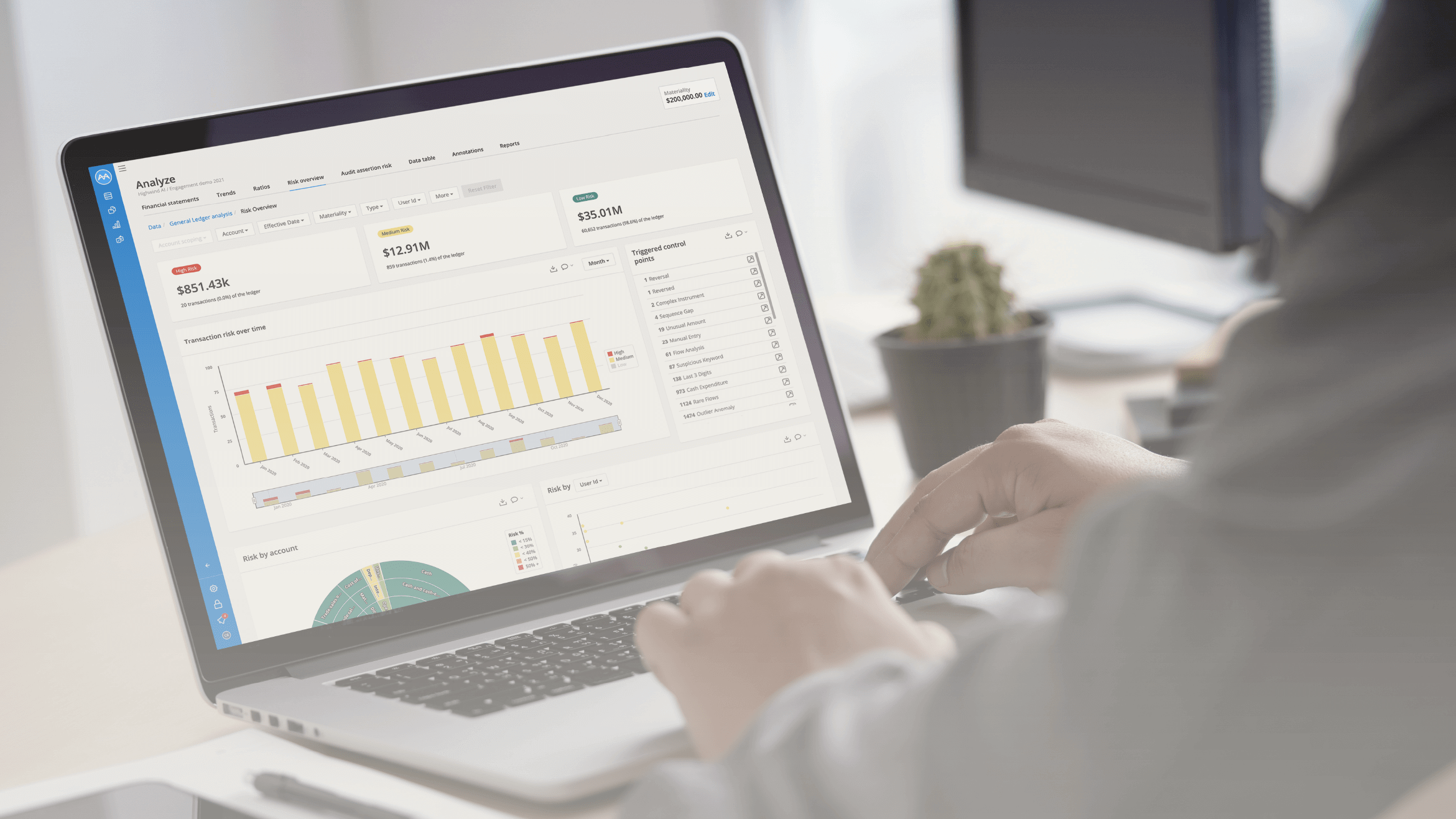

MindBridge’s continued innovation in transaction risk analysis

MindBridge leads in AI-driven anomaly detection, transforming data into insights and tackling human error in financial processes for better efficiency.

MindBridge leads in AI-driven anomaly detection, transforming data into insights and tackling human error in financial processes for better efficiency.

Upon its launch in 2022, ChatGPT single-handedly took “AI” from a futuristic concept to reality – and to the top of the agenda for many finance professionals. For the first time in a long time, there is the promise of transformational technology in the finance department. There is only one crucial issue: ChatGPT and its … Read more

Explore the transformative role of AI in Audit and Finance with key takeaways from IIA GAM 2024. See how MindBridge AI leads the charge in audit innovation.

Discover generative AI’s impact on finance and accounting trends, including automation, digital transformation, and how it revolutionizes the industry.

We are pleased to announce that MindBridge has successfully obtained/renewed its cloud security compliance standards.

We’re incredibly excited to announce that MindBridge has been included in the Vector Institute’s inaugural AI20 for 2023. Read more in the Press Release published here. With over 1,200 artificial intelligence-focused firms in Canada, receiving this recognition alongside a select group of leading Canadian AI organizations is a testament to the value we consistently deliver … Read more

Unbiased AI is a goal we all want to achieve, but it’s continuously difficult when dealing with human-centric technology.

This guide covers how the international standards addressing technology ethics and bias in auditing affect organizational tech use.

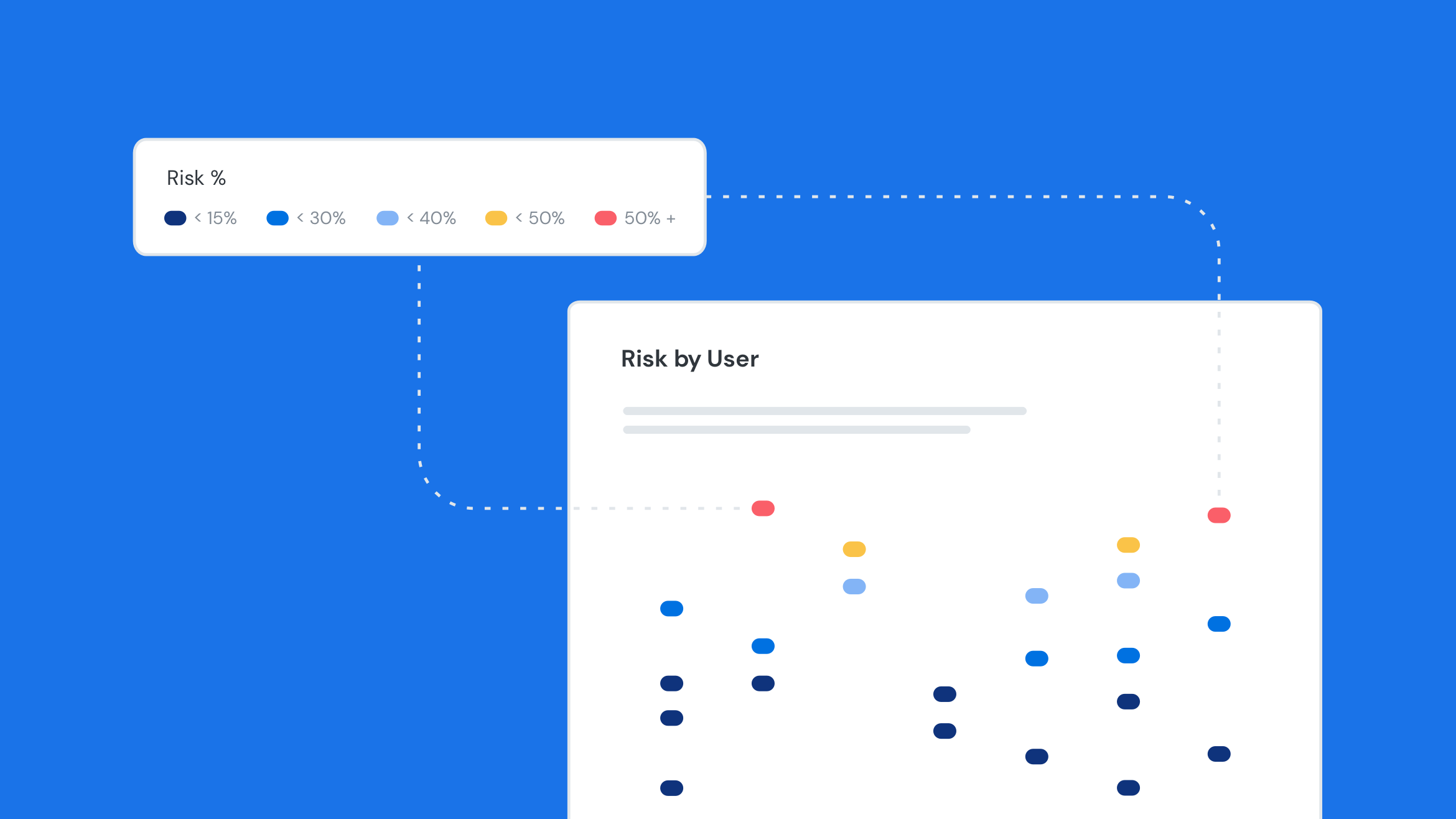

As the complexity of data analysis increases, preemptive vs. reactionary capabilities become paramount. Data anomaly detection can help.

Human-centric AI for anomaly detection is designed to use human input to help support and scale financial risk discovery objectives.

Anomaly detection is a powerful technique for detecting fraudulent transactions and behaviors, thanks to financial institutions’ ever-increasing amounts of data.

This webinar will provide a pathway to enable use of the best technologies and procedures necessary to reduce the overall risk of fraud.