An effective audit starts with a solid audit plan. While the overall audit strategy and plan can vary between clients, an auditor will usually establish risk assessment procedures and a how-to response for the risk of material misstatement.

The challenge is that sometimes, even the most thorough and comprehensive audit plans can still have gaps. In fact, every auditor understands there will likely always be some degree of uncertainty and unidentified risks before an audit begins. It’s in the initial audit planning stages that an audit team will often ask:

- How can we lessen those unknown risks?

- Is there an opportunity to confirm initial assessments about the industry or company?

- Are there blind spots that we haven’t considered?

This is where machine learning (ML) and artificial intelligence (AI) can help. In this blog, you’ll learn how you can use MindBridge AI to spot risks and shift resources during preliminary engagement activities through each phase of the audit planning process.

Pinpointing audit risks using a data-driven method

Identifying the inherent business risks associated with the company is an important first step in the audit planning process. An auditor must analyze key risk factors such as understanding the industry risks, the company’s business, and any recent changes within the company to determine if and how these considerations will impact the audit plan.

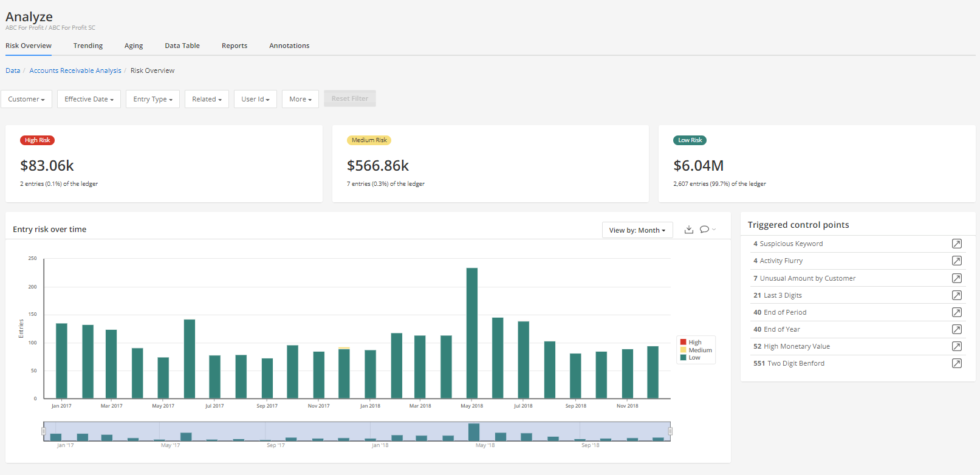

Using Ai Auditor, an audit team can enhance the risk assessment process by retrieving powerful risk insights. That’s because Ai Auditor examines 100% of the company’s transaction data and alerts the team to any anomalies or underlying risks associated with the entity. With detailed data at-hand, the audit team can then move forward with greater confidence in the audit engagement, trusting that the risk assessment is comprehensive and complete.

Ai Auditor can also help the team to identify new risk areas that have might not been flagged in previous audits and include them in their audit plan. Not only does this ensure a well-planned audit, but it also minimizes the potential for duplicating audit procedures later on.

Evaluating the effectiveness of the company’s internal control over financial reporting is another area where using Ai Auditor can be a benefit. Much like traditional testing, the platform automatically identifies control points to spot high-risks transaction data. The auditing team can also adjust these control points and use other capabilities within the platform to recreate traditional control testing models. This data-driven audit method saves the team time while ensuring high levels of accuracy and diligence.

Building an effective audit strategy with Ai Auditor

After initial risk assessments and tests, the auditors will be able to establish an overall audit strategy. This sets the scope, timing, and direction of the audit and guides the development of the audit plan.

For instance, the audit team will derive important conclusions after evaluating the effectiveness of internal control over financial reporting. These will help them decide whether to use control testing, substantive testing, or a combination of both in their audit plan.

When planning the timing of the audit, the team might also consider using Ai Auditor during interim analysis and take advantage of roll-forward capabilities at year-end to ensure a more effective audit.

Considering how much time and resources go into an audit, Ai Auditor can become a force-multiplier for an audit team. The platform provides insights that help them become more efficient as they move through audit planning to engagement completion.

Developing an audit plan with data at your fingertips

As an auditor begins developing and documenting the audit plan, the reporting features within Ai Auditor can help. An auditing team can export powerful graphs and data to support the audit plan regarding details such as the planned nature, timing, and extent of the risk assessment procedures; the planned nature, timing, and extent of tests of controls and substantive procedures; and other planned audit procedures.

The team can also use Ai Auditor to download a single report that details any flagged items and automatically add this report to the audit plan. This ensures the team conducts deeper investigations on those transactions or simply helps to justify why certain samples were selected.

Completing the audit engagement with success

Ai Auditor helps to simplify auditing planning. The platform offers valuable insights and data that help an auditing team streamline risk assessments, build an effective strategy, and outline a comprehensive audit plan. And since an audit team will be able to conduct investigations easier and faster through every phase of the plan’s process, they’ll have more time to offer clients valuable insights and guidance.

Looking for more? Register to access our on-demand webinar titled ‘Riding the Waves of Transformation’ with Tom Hood, CPA.