Due to historical computing power limitations, the risk assessment process has been a theoretical exercise that lacked actual data representing current year operations. Leveraging new technologies, such as MindBridge, auditors are now able to introduce data earlier in the audit process. The actual data of the current period helps shape and deepen an auditor’s understanding of the entity.

The results can be used to visualize and interpret the transactional detail to reassess how you are calculating the risk of material misstatement, build unbiased audit evidence, enhance line of questions for clients and create more depth your understanding of the entity. This is critical to enhancing the efficiency and quality of your engagement because

How MindBridge can help

Introducing a new approach to Risk Assessment from MindBridge.

Download our resource that helps audit professionals better understand the correlation and usability of MindBridge as it relates to the Statement on Auditing Standards (SAS) No. 145 titled Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement issued by the AICPA Auditing Standards Board (ASB). ”

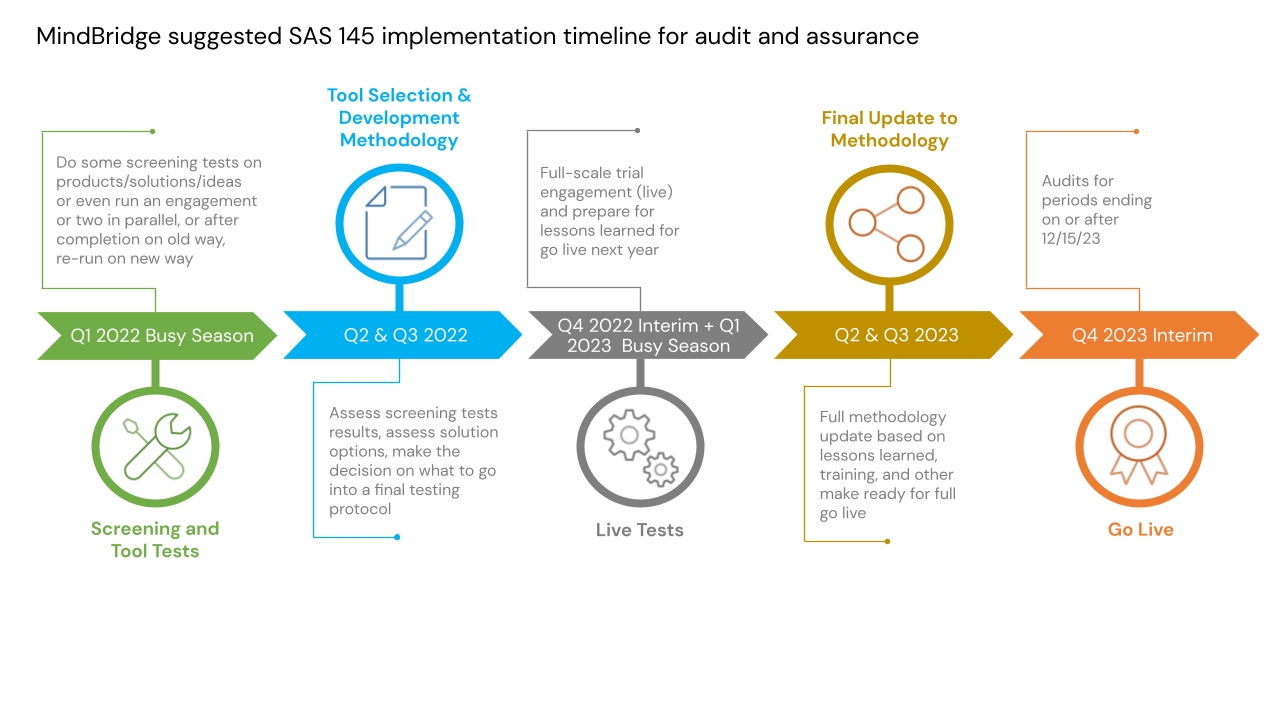

Suggested firm implementation timeline

SAS No. 145 is effective for audits of financial statements for periods ending on or after December 15, 2023. Early implementation is permitted.

The new MindBridge guide provides various approaches to assist the auditor in leveraging advanced data analytics in the risk of material misstatements as well as other uses related to creating more depth of the auditor’s understanding of the entity. This guide can also be used for ISA 315 revised 2019, and AS 2110.

For technical assistance or to discuss further with our Methodology Team, contact your MindBridge Support Representative, or reach us at info@mindbridge.ai.